'Correction Territory'

'Correction Territory'

Today's Daily Briefing

Know someone who would like this newsletter? Forward it to them.

The World

President Vladimir V. Putin ordered Russian troops into Ukraine but made clear his target goes beyond his neighbor to America’s “empire of lies,” and he threatened “consequences you have never faced in your history” for “anyone who tries to interfere with us.” In a speech early Thursday, full of festering historical grievances and accusations of a relentless Western plot against his country, Mr. Putin reminded the world that Russia “remains one of the most powerful nuclear states” with “a certain advantage in several cutting edge weapons.” In effect, Mr. Putin’s speech, intended to justify the invasion, seemed to come close to threatening nuclear war. (New York Times)

Economic fallout: Dow enters correction territory as the crisis roils markets: U.S. and European stocks fell sharply, shares in Moscow plunged, the rouble hit a record low, traders piled into low-risk government debt, oil hits $105 a barrel, and gold hit a 17-month high after Russia’s invasion of Ukraine. (Financial Times)

China: China is ready to throw Russia an economic lifeline as Vladimir Putin’s ties with the west deteriorate and Moscow is hit by snowballing sanctions over the crisis in Ukraine. Financial analysts and geopolitical experts believed China would probably help Russia weather those sanctions, mostly through resource deals and lending by several state-owned banks, while seeking to avoid damage to its own economic and financial interests. “The level of Chinese support for Russian actions could be an influential factor in shaping an evolving crisis,” said Tom Rafferty, a Beijing-based analyst with the Economist Intelligence Unit. (Financial Times)

Cyber: The Lloyds Banking Group chief Charlie Nunn said the bank is “on heightened alert” for any cyberattack from Russia. (The Times)

Geopolitics: Russia’s audacious military assault on Ukraine is the first major clash marking a new order in international politics, with three major powers jostling for position in ways that threaten America’s primacy. The challenges are different than those the U.S. and its network of alliances faced in the Cold War. Russia and China have built a thriving partnership based in part on a shared interest in diminishing U.S. power. Unlike the Sino-Soviet bloc of the 1950s, Russia is a critical gas supplier to Europe, while China isn’t an impoverished, war-ravaged partner but the world’s manufacturing powerhouse with an expanding military. In deploying a huge force and on Thursday ordering what he called a “special military operation,” Russian President Vladimir Putin is demanding that the West rewrite the post-Cold War security arrangements for Europe and demonstrated that Russia has the military capability to impose its will despite Western objections and economic sanctions. (Wall Street Journal)

President Macron will start his run for a second term within days and hold a rally on March 5 to launch a five-week campaign that will cast him as a reliable statesman against a field of mediocre contenders. Aides confirmed that the 44-year-old president will descend from the Elysée Palace into the campaign ring close to the March 4 deadline after delaying to devote time to mediating in the Ukraine crisis. (The Times)

Google’s real estate VP told San Francisco Bay Area employees that Covid-19 risk has fallen low enough to reinstate the buzzy, fun perks for which the company is known, such as fitness centers and massages. The regional offices are also dropping some of the Covid-19 protocol requirements, and the company will no longer require vaccination as a condition of employment in the U.S. It comes as the company prepares to bring workers back to the office three days a week after two years of delays. (CNBC)

L.A. County bars, offices, gyms can drop mask rules with COVID vaccine verification. The revised rules take effect 12:01 a.m. Friday and will make masking optional indoors in certain settings that screen the vaccination status of patrons. (Los Angeles Times)

Say hello again to the office, fingers crossed: The two-year mark since many American businesses sent their office workers home is approaching, and some antsy executives have delivered a long-delayed message: Return-to-office plans are real this time (fingers crossed). Managers are hanging up welcome balloons and dusting off monitors with a sense of confidence. Coronavirus tests are widely available, including some provided by employers. Many businesses know the majority of their employees are vaccinated. Many workers have recovered from Omicron and are resuming indoor social activities. Executives are entering the next zone of return-to-office planning with what psychologists call “stress-related growth.” They have endured a sustained period of tumult. They are emerging feeling hopeful, equipped with new insights about how to respond when Covid cases surge and how to keep workers safe while businesses are open: by encouraging testing and imposing vaccine rules. (New York Times)

Buffett’s dealmaking slump forces a new reality on Berkshire: Berkshire Hathaway's annual letter and earnings are set for release on Saturday morning. (Bloomberg)

Economy

Bitcoin prices and other cryptocurrencies tumbled after Russia attacks Ukraine. Bitcoin fell to a one-month low on Thursday with other cryptocurrencies including ether plunged. More than $150 billion has been wiped off the entire cryptocurrency market in the last 24 hours. (CNBC)

Russia could use cryptocurrency to blunt the force of U.S. sanctions: Russian companies have many cryptocurrency tools at their disposal to evade sanctions, including a so-called digital ruble and ransomware. (New York Times)

Stablecoin market caps have reached ~$180B, up from ~$38B a year ago, as bitcoin, ether, and others fluctuate wildly. (Bloomberg)

Wintershall Dea, one of the main European investors in the Nord Stream 2 gas pipeline, said it expected to be compensated for the €730mn it has invested in the project if the fallout from Russia’s invasion of Ukraine prevented it from becoming operational. (Financial Times)

The number of Americans filing new claims for unemployment benefits fell slightly more than expected last week, indicating that the labor market recovery was gaining traction. The weekly jobless claims report from the Labor Department on Thursday also showed unemployment rolls shrinking to levels last seen in 1970, underscoring the tightening labor market conditions. (Reuters)

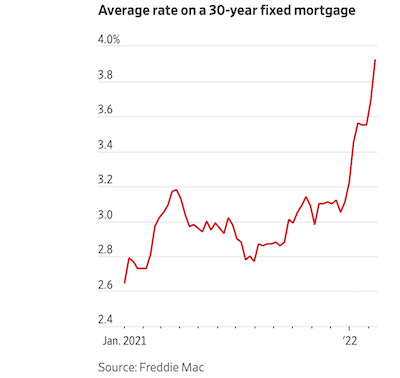

Mortgage rates hovered just below 4% for a second week, maintaining stress on potential buyers facing high prices and low inventory. The average rate for a 30-year fixed-rate loan was 3.89%, mortgage-finance giant Freddie Mac said Thursday, down slightly from 3.92% last week. At the beginning of the year, the average rate on America’s most popular home loan was 3.22%. The Russian invasion of Ukraine stands to push down mortgage rates as investors flock to U.S. Treasurys. (Wall Street Journal)

Bank of America’s co-head of global capital markets in Asia-Pacific is leaving Hong Kong after less than two years as harsh pandemic restrictions prompt an exodus of executives from the territory. Craig Coben, who moved to Hong Kong in 2020 after 15 years at the bank in the US and London, will return to his home in London and retire from the bank. Coben is the most senior departure from the Wall Street bank’s Asia headquarters as more than two years of travel restrictions and severe quarantines force global businesses to reconsider their operations in Hong Kong. (Financial Times)

Inflation is creeping into Asian nations like Japan and India. High energy and food prices are beginning to influence countries that recently seemed immune to cost pressures. (The Wall Street Journal)

The Federal Reserve puts new bans on trading in stocks, bonds, crypto or commodities following a trading scandal. Notably, officials are able to hold existing stocks, but cryptocurrencies are off-limits. (The Block)

Technology

Semiconductor shortage produces record venture funding: While most of the talk around semiconductors revolves around disruptions in the supply chain, the industry actually saw an unprecedented amount of venture capital in 2021—as well as one of its biggest M&A years ever. (Crunchbase)

Reddit launched the first major change to its mobile app in over two years with the addition of a new Discover Tab, offering personalized recommendations, as well as a revamped navigation system that includes new Community and Profile menus where users can quickly access and reorganize their subscriptions or access their profile settings. The company said it heard from users that they wanted a better way to explore their interests, which prompted the decision to introduce the Discover Tab.

Reddit today has over 100,000 active communities, but many of them are still under-exposed. (TechCrunch)

AirTags are linked to stalking, and Apple needs to cooperate with Google, Samsung, Tile and others to resolve the issue. (CNET)

Meta is testing an artificial intelligence system that lets people build parts of virtual worlds by describing them, and CEO Mark Zuckerberg showed off a prototype at a live event today. Proof of the concept, called Builder Bot, could eventually draw more people into Meta’s Horizon “metaverse” virtual reality experiences. It could also advance creative AI tech that powers machine-generated art. In a prerecorded demo video, Zuckerberg walked viewers through the process of making a virtual space with Builder Bot, starting with commands like “let’s go to the beach,” which prompts the bot to create a cartoonish 3D landscape of sand and water around him. (The Verge)

Smart Links

Pay hikes fail to lure millennials back to work in Fed study. (Bloomberg)

Samsung shipped '100 million' phones with flawed encryption. (The Register)

Renting a car is still going to be hard this summer. (Wall Street Journal)

MLS inks metaverse partnership. (Axios)

Texas spurs copycats as states punish banks that snub oil and gas. (Bloomberg)