Spending Spigot

The World

The U.S. economy contracted at a record rate last quarter and weekly jobless claims rose for the second straight week. The Commerce Department said U.S. GDP fell at a 32.9% annual rate in 2Q20, a 9.5% drop compared with the same quarter a year ago. Both figures were the steepest in records dating to 1947. Separately, the Labor Department said weekly unemployment benefits applications rose to 1.43 million, while the number of people receiving unemployment benefits increased by 867,000 to 17 million, signs the jobs recovery is losing momentum. (Wall Street Journal)

Fed Chair Jay Powell said urgency is growing for lawmakers to reopen their spending spigot to rescue the economy. Meanwhile, Congressional relief plan talks are “a mess,” as the parties remain trillions of dollars apart, while U.S. small businesses face mass closures without more aid. (Finance 202, Washington Post, Reuters)

Germany’s economy shrank the most in at least half a century in 2Q20. The 10.1% drop in output in the region’s largest economy is a harbinger of worse figures elsewhere, as Spain, France and Italy likely will report even deeper contractions tomorrow. Spanish banking giant Santander has reported a record €11.1 billion quarterly loss after taking big writedowns on its British and international businesses, and the UK car industry produced the lowest number of vehicles in 1H20 since 1954. Meanwhile, European airline and airport executives urged the Canadian government this week to allow a safe “restoration of travel” between Canada and Europe. (Yahoo Finance, The Times, The Guardian, Reuters)

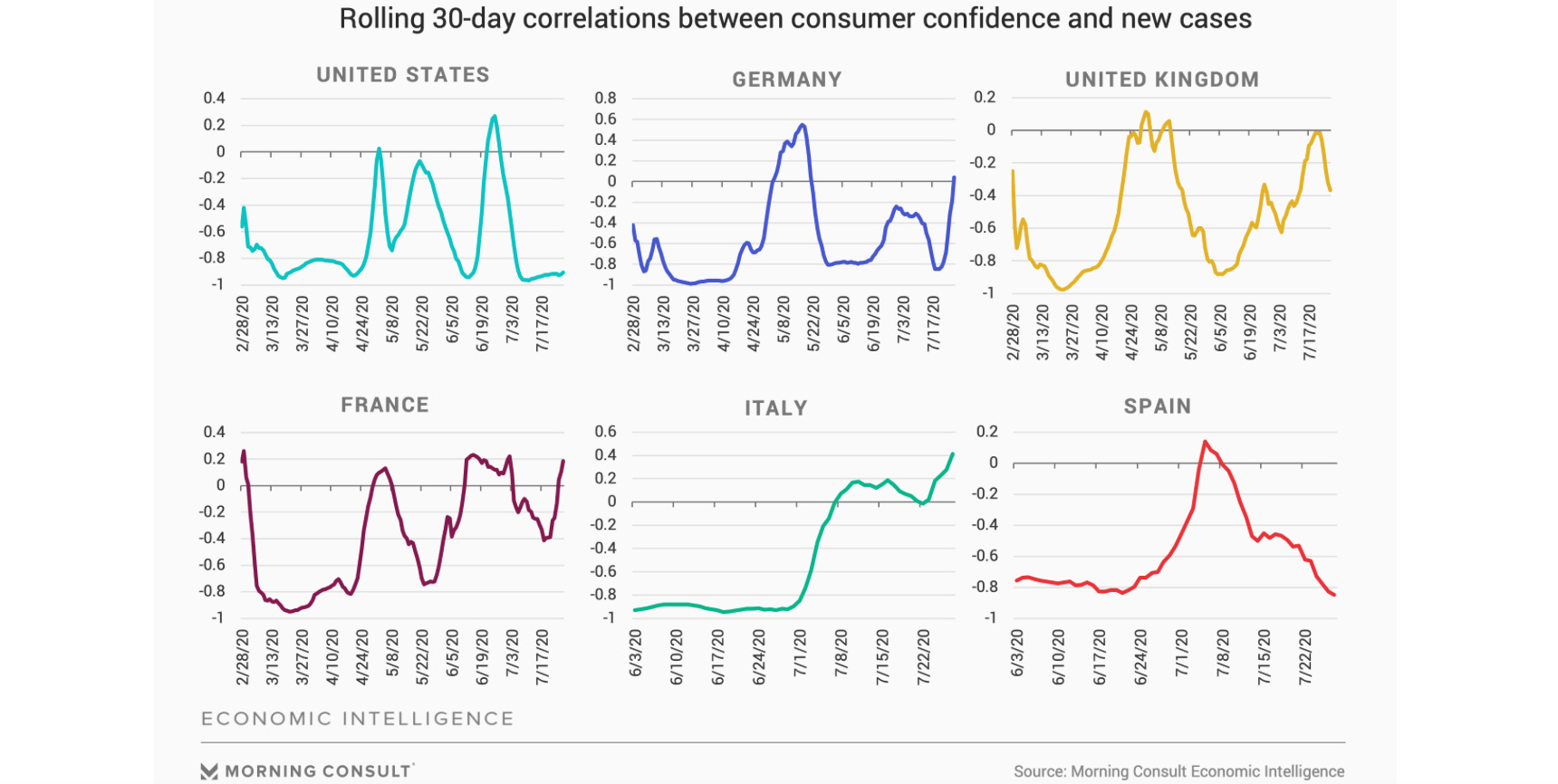

After moving in lockstep during the pandemic’s early stages, consumer confidence in the U.S. and Europe resumed taking opposite paths, raising questions whether an economic recovery is possible without a meaningful reduction in cases. (Morning Consult)

The commander of American forces in Japan said the U.S. is fully committed to help Tokyo handle China's repeated incursions into waters surrounding the Senkaku Islands. Meanwhile, India has tightened restrictions on Chinese companies seeking to supply goods or services to the government, expanding its economic retaliation against Beijing, as China is being urged to develop its own international payment system to counter risk of US financial sanctions. (Nikkei Asian Review, Caixin Global, South China Morning Post)

Four of the big U.S. tech firms, accounting for nearly a fifth of the S&P 500’s total value, report results today — the first time Apple, Amazon, Alphabet, and Facebook post financial results on the same day. Meanwhile, yesterday’s Congressional hearing showed that the effort to regulate tech companies is becoming a big-tent issue, and possibly a place for compromise between conservatives worried largely about constraints on their speech, and liberals worried primarily about constraints on competition. (Reuters, Wall Street Journal)

Economy

Zillow said 90% of its 5,400-person workforce may never have to come back into the office, announcing a “flexible work-from-home policy,” even once it is safe to go back to offices. Long term, employees can “work where they are most productive, whether that is in the office, their home, or a combination of both.” (The Information)

The global crisis may be an opportunity for private equity: In times of crisis, private equity funds provide their companies with liquidity, which gives them an advantage over competitors. (Calcalist)

BCG lists the most innovative companies in the world: Tech companies unsurprisingly dominated the top end of the 2020 ranking, with Apple jumping two spots from 2019’s ranking to reach #1, Alphabet dropping one spot to #2, and Amazon dropping one spot to #3. Microsoft and Samsung remained in fourth and fifth place, respectively. Remaining a serial innovator is a trying task, with only eight companies consistently cracking BCG’s top 50 ranking for the last 14 years: Alphabet, Amazon, Apple, HP, IBM, Microsoft, Samsung, and Toyota. Of the 162 companies on the list in the last 14 years, 30% have appeared just once and 57% have appeared three times or fewer. The BCG report noted that the most innovative firms have an aligned strategy and significant innovation investment. Of the 1,000+ companies surveyed by the consulting firm, 45% were “committed innovators” who said that innovation was a top priority and supported it with significant investment. “Skeptical innovators” (30%) viewed innovation as neither a strategic priority nor an important funding target. “Confused innovators” (25%) had a mismatch between how they viewed the strategic importance of innovation and their level of investment. The financial and pharma sectors had the largest proportion of committed innovators (56%), while wholesale and retail had the lowest share (32%). Being a committed innovator pays dividends, the report found. 60% of committed innovators saw a rising proportion of sales from products and services launched in the past three years, compared to 30% of skeptics and 47% of confused innovators. With every industry becoming a tech industry to some degree, boundary-crossing innovation is becoming an increasingly important capability. BCG says that we are seeing much more cross-industry innovation, with such activity increasing by 20% from 2016. Finally, successful serial innovators get three things right: (BCG, Forbes, Consulting.US)

They “Walk the Talk”: Innovation success starts with commitment—making innovation a priority and investing decisively behind that ambition.

They Embrace the Benefits of Scale

They Calibrate Their Innovation Systems for Success

Technology

Google and Samsung are negotiating a major deal that would give Google products more prominence on the South Korean company’s smartphones. The talks involve giving Google more control over search on Samsung handsets globally. (Bloomberg)

Spotify said customers’ overall time spent listening returned to prepandemic levels and its advertising business is showing signs of recovery, while reporting a €356 million 2Q20 loss despite an increase in paying subscribers. (The Verge)

Elon Musk says Tesla is open to licensing its software Autopilot, as well as supplying powertrains and batteries to other automakers. (TechCrunch)

Rep. David Cicilline (D-R.I.), who chaired yesterday's Big Tech hearings, said Facebook should be broken up, in part because of its acquisitions of Instagram and WhatsApp: "Mr. Zuckerberg acknowledged in this hearing that his acquisition of WhatsApp and Instagram were part of a plan to both buy a competitor and also maintain his money, power, or his dominance. That's classic monopoly behavior." (Axios)

Smart Links

5 ways to stabilize the COVID-19 economy. (MIT Sloan)

Huawei overtakes Samsung as world’s biggest smartphone vendor. (Canalys)

U.S. median home asking price hits all-time high. (Mansion Global)

U.S. Edtech raises $803M in 1H20. (EdSurge)

Restaurants are banding together to chase insurance companies for denied pandemic claims. (Zagat)

Golf: 2020 U.S. Open will be held without fans at Winged Foot in September. (CBS Sports)